Permanent and variable Working Capital

Permanent and Variable Working Capital

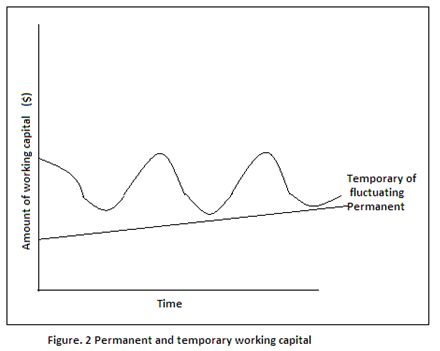

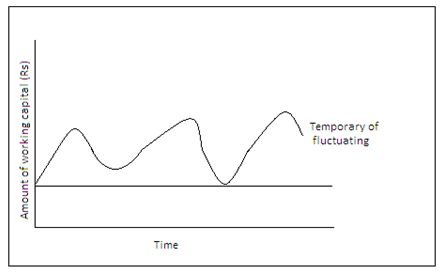

We know that the need for current assets arises because of the operating cycle. The operating cycle is a continuous process and, therefore, the need for current assets is felt constantly. But the magnitude of current assets needed is not always the same; it increases and decreases over time. However, there is always a minimum level of current assets which is continuously required by a firm to carry on its business operations. Permanent or fixed, working capital is the minimum level of current assets. It is permanent in the same away as the firm’s fixed assets. It is permanent in the same way as the firm’s fixed assets are. Depending upon the changes in production and sales, the need for working capital, over and above permanent working capital, will fluctuate. For example, extra inventory of finished goods will have to be maintained to support the peak periods of sale, and investment in debtors (receivable) may also increase during such periods, On the other hands, investment in raw material, work-process and finished goods will fall if the market is slack.

Figure 1. Permanent and temporary working capital.

Fluctuating or Variable working capital is the extra working capital needed to support the changing production and sales activities of the firm. Both kinds of working capital permanent and fluctuating (temporary) – are necessary to facilitate production and sale through the operating cycle. But the firm to meet liquidity requirements that will last only temporarily creates the temporary working capital. Figure 1. Illustrates difference between permanent and temporary working capital. If is shown that permanent working capital is stable over time, while temporary, working capital is fluctuating sometimes increasing and sometimes decreasing. However, the permanent working capital line need not be horizontal if the firm’s requirement for permanent capital is increasing (or decreasing ) over a period. For a growing firm the difference between permanent and temporary working capital can be depicted through figure 2.